What Is Gap Insurance? Protect Yourself When Your Car Is Totaled

You’ve just driven your brand-new car off the dealership lot. That new car smell fills the cabin, the odometer reads 12 miles, and you’re beaming with pride. But here’s a reality check that most buyers don’t think about: your car just lost thousands of dollars in value the moment you left the lot.

Now imagine this scenario six months later: you’re stopped at a red light when another driver plows into the back of your car, totaling it completely. Your insurance company cuts you a check for $22,000, the current market value of your now-destroyed vehicle. Sounds fair, right?

Not quite. You still owe $27,000 on your loan. Suddenly, you’re $5,000 in the hole for a car you can’t even drive anymore.

This nightmare scenario is exactly why gap insurance exists, yet surveys show that nearly 60% of American car buyers don’t fully understand what it is or whether they need it. If you’re asking yourself “what is gap insurance” or “do I need gap insurance,” you’re not alone, and you’re asking the right questions at the right time.

In this comprehensive guide, we’ll break down everything you need to know about gap coverage car insurance: what it is, how it works, who needs it, what it costs, where to buy it, and most importantly, whether it makes financial sense for your specific situation. By the end, you’ll have the clarity to make an informed decision that could save you thousands of dollars or protect you from financial disaster.

Let’s dive in.

What is Gap Insurance? The Complete Definition

Understanding Gap Insurance Basics

GAP stands for Guaranteed Asset Protection, though many insurance professionals simply call it “gap insurance” or “gap coverage.”

Here’s the simple definition: Gap insurance is optional coverage that pays the difference between what your car is worth (its actual cash value) and what you still owe on your auto loan or lease if your vehicle is totaled or stolen.

Let’s break this down with real numbers to make it crystal clear.

A Real-World Gap Insurance Example

Your situation:

- You bought a new 2024 Honda Accord for $32,000

- You put $2,000 down and financed $30,000 at 6% for 72 months

- Your monthly payment is $497

After 12 months:

- You’ve paid down your loan to $26,500 (remaining balance)

- Due to depreciation, your car’s actual cash value is now $23,000

- Your “gap” = $3,500

Then disaster strikes: A tree falls on your parked car during a storm, totaling it.

Without gap insurance:

- Your regular auto insurance pays you $23,000 (the car’s current value)

- You still owe the lender $26,500

- You must pay $3,500 out of pocket for a car you no longer have

- You still need to buy another car

With gap insurance:

- Your regular auto insurance pays $23,000

- Your gap insurance pays the remaining $3,500

- Your loan is completely paid off

- You walk away even, ready to purchase another vehicle without that debt hanging over you

That $3,500 difference? That’s the “gap” that gap insurance covers.

Why the Gap Exists: The Depreciation Reality

New vehicles depreciate rapidly; it’s an unavoidable fact of car ownership. Here are the harsh realities:

Typical new car depreciation:

- Immediately upon purchase: 9-11% value loss

- After one year: 20-30% total depreciation

- After three years: 40-50% total depreciation

- After five years: 60% or more total depreciation

Meanwhile, your loan balance decreases much more slowly, especially in the early years when most of your payment goes toward interest. This creates a dangerous gap where you owe significantly more than the car is worth.

Example depreciation timeline for a $35,000 vehicle:

| Time | Car’s Value | Loan Balance | Gap |

|---|---|---|---|

| Day 1 | $31,500 | $35,000 | $3,500 |

| 6 months | $28,000 | $32,800 | $4,800 |

| 12 months | $26,250 | $29,500 | $3,250 |

| 24 months | $22,750 | $23,100 | $350 |

| 36 months | $19,250 | $16,400 | $0 (positive equity) |

Notice how the gap is largest in the first 12-18 months, then gradually closes as the loan balance decreases and depreciation slows.

What Gap Insurance Does NOT Cover

It’s crucial to understand the limitations. Gap coverage car insurance does NOT pay for:

- Your deductible: You’re still responsible for your collision or comprehensive deductible

- Extended warranties or service contracts: Rolled into your loan but not covered by gap

- Additional charges: Late fees, past-due payments, or penalties on your loan

- Mechanical breakdowns: Gap only covers total loss from accidents or theft

- Negative equity from a previous trade-in: If you rolled old debt into your new loan

- Rental car costs or alternative transportation

- Personal belongings were stolen from the vehicle

- Non-factory equipment or custom modifications (wheels, stereo systems) unless specifically included

- Lease penalties or early termination fees (though some gap policies specifically for leases may include this)

Gap insurance is narrowly focused: it pays the difference between insurance settlement and loan balance when your car is totaled or stolen, nothing more, nothing less.

How Does Gap Insurance Work? The Claims Process

When Gap Insurance Kicks In

Gap insurance only activates when your vehicle is declared a total loss. This happens when:

- Accident damage exceeds repair cost: If repairs would cost more than the car’s value (typically 70-80% of value)

- Vehicle is stolen and not recovered: After your insurance company’s waiting period (usually 30 days)

- Weather damage: Flood, hail, fire, or other comprehensive coverage events that total the vehicle

- Vandalism: Severe enough to make repair uneconomical

Important: Minor accidents, fender benders, or repairable damage don’t trigger gap coverage. Your car must be deemed a total loss by your insurance company.

Step-by-Step: How a Gap Insurance Claim Works

Let’s walk through the actual process:

Step 1: Total Loss Determination. Your regular auto insurance company (State Farm, Geico, Progressive, etc.) inspects the damage and declares your vehicle a total loss.

Step 2: Insurance Settlement Your insurance company calculates your car’s actual cash value (ACV) and offers a settlement. They’ll deduct your deductible from this amount.

Example settlement:

- Car’s actual cash value: $24,000

- Your comprehensive deductible: $500

- Insurance payout to you: $23,500

Step 3: Determine the Gap. Find out your exact loan payoff amount from your lender (not just the balance, ask for the “payoff amount” which includes any fees or interest through the payoff date).

Example:

- Loan payoff amount: $28,200

- Insurance payout: $23,500

- Gap: $4,700

Step 4: File Gap Insurance Claim. Contact your gap insurance provider (might be your auto insurer, the dealership, or a separate company) and provide:

- Copy of your insurance settlement check or letter

- Loan payoff statement from your lender

- Original loan or lease agreement

- Title or registration

Step 5: Gap Insurance Payment After reviewing your claim (typically 5-15 business days), the gap insurer pays the difference directly to your lender.

In our example:

- Gap insurance pays: $4,700

- Your lender receives: $23,500 (from auto insurance) + $4,700 (from gap) = $28,200

- Your loan is completely satisfied

Step 6: Any Refund to You. If your insurance settlement plus gap payment exceeds your loan payoff, you receive the difference. If there’s negative equity you’re still responsible for (like rolled-in previous debt), you may still owe something.

Timeline Expectations

Typical gap claim timeline:

- Total loss declaration: Immediate to 7 days after accident/theft

- Insurance settlement: 7-21 days

- Gap claim filing: Immediately after receiving the insurance settlement

- Gap payment: 5-15 business days after filing

- Total process: 3-6 weeks typically

Pro tip: Don’t make any payments on the totaled car’s loan after the loss date. Gap insurance calculates based on the payoff amount as of the loss date, not when the claim is processed.

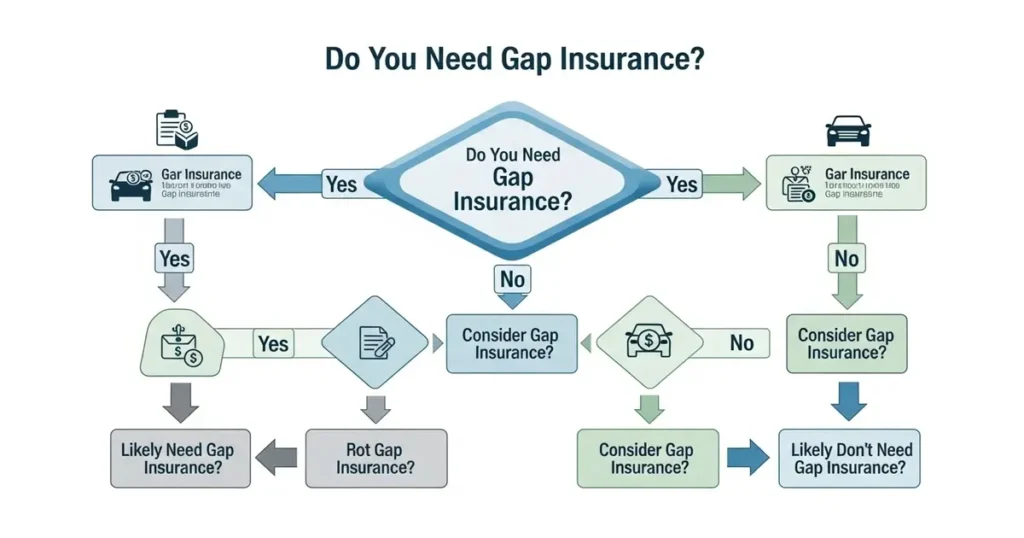

Do I Need Gap Insurance? 7 Situations Where the Answer is YES

Situation 1: You Made a Small Down Payment (Less Than 20%)

Why it matters: The less you put down, the more you finance, and the bigger the immediate gap between what you owe and what the car is worth.

The math:

- Vehicle price: $30,000

- Down payment (5%): $1,500

- Amount financed: $28,500

- Car’s value driving off lot: ~$27,000

- Immediate gap: $1,500+ (and it grows from there)

You definitely need gap insurance if you put down:

- Less than 10% on a new car

- Less than 20% on a used car

- $0 down (very high risk)

Real example: Tyler bought a $28,000 Toyota Camry with zero down (dealer promotion). Within three months, his car was totaled when someone ran a red light. His insurance paid $24,500. He owed $27,200. Gap insurance saved him from a $2,700 debt on a car he couldn’t drive.

Situation 2: You Have a Long-Term Loan (60+ Months)

Why it matters: Longer loans mean slower payoff rates. Your car depreciates faster than your balance decreases, creating and maintaining a significant gap for years.

The 72-month loan trap: With increasingly popular 72-84 month loans, you’re underwater for potentially 4-5 years. This dramatically extends your risk period.

Comparison:

- 36-month loan: Underwater for ~18 months

- 48-month loan: Underwater for ~24 months

- 60-month loan: Underwater for ~30-36 months

- 72-month loan: Underwater for ~42-48 months

- 84-month loan: You might be underwater the entire term

Reality check: According to Experian’s State of the Automotive Finance Market, the average new-car loan term is now 68 months, and nearly 40% of new-car loans are 72+ months. If this describes your loan, you need gap insurance.

Situation 3: You Financed More Than 100% of the Vehicle’s Value

Why it matters: If you rolled negative equity from a trade-in into your new loan, you started out owing more than the car’s worth—before it even began depreciating.

How this happens:

- You trade in a car worth $12,000

- You still owe $15,000 on that trade-in

- You have $3,000 negative equity

- This $3,000 gets added to your new car loan

- You’re $3,000 underwater before driving an inch

The compounding problem: Now your new car depreciates while you’re paying off debt from a car you no longer own.

Example scenario:

- New car price: $32,000

- Negative equity rolled in: $4,000

- Total financed: $36,000

- Car’s actual value: $32,000 → $28,800 after one year

- Loan balance after one year: $33,500

- Gap: $4,700

If you rolled in any negative equity, gap insurance isn’t optional—it’s essential.

Situation 4: You Bought or Leased a New Vehicle

Why it matters: New cars depreciate fastest in the first year (20-30%), while your loan balance barely budges. This creates the perfect storm for a significant gap.

New car depreciation shock:

- A $35,000 new car loses $3,500-3,800 the moment you drive away

- After 12 months, it’s worth $24,500-28,000

- Your loan balance might only drop to $31,500

- You’re $3,000-7,000 underwater

For leased vehicles: Gap coverage is often included (but not always), or you’re required to purchase it. Check your lease agreement carefully.

Industry data: The average new car buyer is underwater for the first 2-3 years of a typical loan term. During this window, gap insurance is crucial protection.

Situation 5: You Bought a Vehicle Known for Fast Depreciation

Why it matters: Some vehicles hold their value better than others. If you bought a model with higher-than-average depreciation, your gap is larger and lasts longer.

Vehicles with high depreciation typically include:

- Luxury sedans (Mercedes, BMW, Audi)

- Electric vehicles (technology changes rapidly, though improving)

- Certain SUVs and trucks with poor reliability ratings

- Vehicles from brands with lower resale value

- Models with frequent redesigns or being phased out

Vehicles with low depreciation (lower gap risk):

- Toyota Tacoma, 4Runner, Tundra

- Honda CR-V, Accord

- Subaru Outback, Forester

- Jeep Wrangler

- Ford F-150

Action step: Before buying, research your vehicle’s depreciation rate on sites like Kelley Blue Book, Edmunds, or Consumer Reports. If projected 3-year depreciation exceeds 45%, strongly consider gap coverage.

Situation 6: Your Credit Score Is Lower (Higher Interest Rate)

Why it matters: Higher interest rates mean more of your monthly payment goes to interest instead of principal, so your balance decreases more slowly.

The interest rate impact:

$25,000 loan for 60 months:

- At 4% interest: Balance after 12 months = $20,850

- At 8% interest: Balance after 12 months = $21,430

- At 12% interest: Balance after 12 months = $22,000

The gap widens: With a 12% rate, you’re paying off principal much slower, extending how long you’re underwater.

If your interest rate is 7% or higher, gap insurance becomes more important because you’re paying down the balance slowly while the car depreciates quickly.

Situation 7: You Can’t Afford a $3,000-$7,000 Surprise Expense

Why it matters: This is the most practical consideration. Do I need gap insurance? Ultimately, it comes down to: can you afford to pay thousands of dollars for a car you no longer have?

Financial reality check: According to the Federal Reserve, nearly 40% of Americans would struggle to cover an unexpected $400 expense. A gap of $3,000-$7,000 could be financially devastating.

Ask yourself:

- Do I have an emergency fund that could cover $5,000+ without hardship?

- Would paying off a gap cripple my finances or force me into credit card debt?

- Can I afford a gap payment AND a down payment on a replacement vehicle?

If the answer to any of these is “no,” gap insurance is worth every penny.

When You DON’T Need Gap Insurance

Situation 1: You Made a Large Down Payment (25%+)

Why you’re safe: A substantial down payment means you start with equity in the vehicle and likely never go underwater, or if you do, only briefly and minimally.

Example:

- Vehicle price: $30,000

- Down payment (30%): $9,000

- Financed: $21,000

- Car’s value driving away: $27,000

- You have positive equity from day one

Guideline: 20%+ down payment significantly reduces gap risk; 30%+ essentially eliminates it for most vehicles.

Situation 2: You Have a Short-Term Loan (36 Months or Less)

Why you’re safe: With aggressive principal paydown, your balance decreases faster than depreciation, so you build equity quickly.

The 36-month advantage: Your monthly payments are higher, but you’re paying mostly principal after the first year. By month 18-24, you likely have positive equity.

If you can afford shorter loan terms, you can probably skip gap insurance, though it’s still an inexpensive piece of mind.

Situation 3: You Bought a Used Car (3+ Years Old)

Why you’re safe: Used vehicles have already experienced their steepest depreciation. Their value stabilizes, so the gap between the loan balance and value is smaller and closes faster.

Depreciation after year 3: Annual depreciation typically drops to 5-10% per year, compared to 20-30% in year one.

Exception: If you’re financing a used car for 72 months with a minimal down payment, you might still benefit from gap coverage. Run the numbers.

Situation 4: You’re Paying Cash or Have Substantial Equity

Why you’re safe: No loan means no gap. Pretty simple.

If you:

- Paid cash outright

- Financed a small amount with a huge down payment

- Own the vehicle free and clear

- Trade-in value exceeds new purchase price

You don’t need gap insurance; there’s no gap to cover.

Situation 5: Your Vehicle Holds Its Value Exceptionally Well

Why you’re safe: Some vehicles depreciate so slowly that the gap never really opens up, even with modest down payments.

Examples of value-holding vehicles:

- Toyota Tacoma (often depreciates only 30% in the first 3 years)

- Subaru vehicles (especially Outback, Forester)

- Honda CR-V

- Jeep Wrangler (sometimes appreciates in certain markets)

- Ford Bronco (high demand models)

Caveat: Market conditions change. Even historically strong vehicles can experience periods of higher depreciation due to economic conditions, fuel prices, or oversupply.

Situation 6: You Have Substantial Savings Specifically for Emergencies

Why you might skip it: If you have $10,000-$20,000 in liquid emergency savings specifically earmarked for unexpected expenses like this, you can self-insure.

The calculation: Gap insurance might cost $400-$700 total. If you can comfortably absorb a $5,000 loss without financial strain, you could skip it and keep that $400-$700.

However, Most financial advisors still recommend gap insurance even if you have savings, because protecting your emergency fund for true emergencies (job loss, medical issues) makes more sense than depleting it for a car gap.

How Much Does Gap Insurance Cost?

Dealership Gap Insurance Costs

Typical pricing at dealerships:

- One-time fee: $400-$700 (average $500-$600)

- Rolled into your loan: Adds to the total financed amount

- Duration: Entire loan term

The dealership markup: Dealerships often mark up gap insurance significantly. They might pay $200-$300 for the policy, but charge you $600-$700; that’s a 100-200% markup.

Red flag: Some dealers charge $900-$1,200 for gap insurance. This is excessive, and you should negotiate or buy elsewhere.

Auto Insurance Company Gap Coverage Costs

Typical pricing from insurers:

- Annual cost: $20-$60 per year (average $40)

- Monthly addition: $3-$5 added to your car insurance premium

- Duration: Typically recommended for the first 3-4 years

Total cost comparison:

- 5 years at $40/year = $200 total

- Versus dealer price of $600 = $400 savings

The catch: You need qualifying comprehensive and collision coverage on your auto policy. If you drop full coverage, you lose gap coverage too.

Credit Union and Bank Gap Insurance

Typical pricing:

- One-time fee: $300-$500

- Annual premium: $25-$40

- Usually less expensive than dealers but more than insurers

Advantage: Credit unions typically offer fair pricing with less markup than dealerships.

Cost Factors That Affect Your Price

Your gap insurance cost depends on:

- Vehicle type: Luxury vehicles or those with fast depreciation cost more

- Loan amount: Higher loan = higher cost

- Loan term: Longer terms increase risk, increasing cost

- Down payment: Smaller down payment = higher risk = higher cost

- Where you buy it: Dealer vs. insurer vs. credit union

- Your state: Insurance regulations vary by state

Is Gap Insurance Worth the Cost? The Math

Average scenario:

- Gap insurance cost: $500 (dealer) or $200 (insurer over 5 years)

- Average gap in total loss: $3,500-$6,000

- Potential savings: $3,000-$5,800

Benefit-to-cost ratio: 7:1 to 12:1 (for every dollar spent, you could save $7-$12)

This is one of the best insurance value propositions in the automotive world.

Compare to other costs:

- Extended warranty: $1,500-$3,000 (often poor value)

- Paint protection: $500-$1,500 (debatable value)

- Gap insurance: $200-$600 (excellent value for high-risk situations)

Where to Buy Gap Insurance: Your 4 Options

Option 1: Car Dealership (Most Expensive, Convenient)

How it works: The finance manager offers gap insurance during the paperwork process, rolling it into your loan.

Pros:

- ✓ Convenient, handled in one transaction

- ✓ No additional approval process needed

- ✓ Coverage starts immediately

- ✓ Can be financed (no upfront cash needed)

Cons:

- ✗ Most expensive option (often 2-3x more than alternatives)

- ✗ High-pressure sales environment

- ✗ You pay interest on the gap insurance cost over the life of your loan

- ✗ Limited ability to shop around in the moment

- ✗ Non-refundable if you refinance or pay off the loan early (in some cases)

Typical cost: $500-$700 (sometimes up to $1,200)

When this makes sense: You’re 100% certain you need it, you’ve negotiated a reasonable price ($400 or less), and you don’t want to deal with another company.

Negotiation tip: Tell the dealer you’ll purchase gap insurance through your auto insurer instead. They’ll often drop the price by 30-50% to keep your business.

Option 2: Auto Insurance Company (Best Value, Recommended)

How it works: Add gap coverage to your existing auto insurance policy as an endorsement or rider.

Where it’s available:

- Progressive

- Nationwide

- Liberty Mutual

- Travelers

- Erie Insurance

- USAA (military families)

- AAA

- Not all insurers offer it (Geico and State Farm don’t in all states)

Pros:

- ✓ Cheapest option ($20-$60/year, $3-$5/month)

- ✓ Can be canceled anytime without penalty

- ✓ Easy to add, just call your agent

- ✓ Proportional refund if you cancel

- ✓ Bundled with auto policy for convenience

- ✓ No interest charges (not financed)

Cons:

- ✗ Requires comprehensive and collision coverage

- ✗ If you drop full coverage, you lose gap coverage

- ✗ Must be added shortly after purchase (usually within 30 days)

- ✗ Not available from all insurers

Typical cost: $20-$60 per year

When this makes sense: This is the best option for most people. Significantly cheaper, flexible, and from a company you already work with.

Action step: Call your insurance agent BEFORE going to the dealership. Get a quote for gap coverage, then decline the dealer’s offer.

Option 3: Credit Union or Bank (Moderate Cost, Good Middle Ground)

How it works: Your lender may offer gap insurance as part of the loan package.

Pros:

- ✓ Usually less expensive than dealer ($300-$500)

- ✓ Fair pricing with less markup

- ✓ Convenient, handled with loan paperwork

- ✓ May offer better terms than dealer policies

Cons:

- ✗ Still more expensive than auto insurers

- ✗ Not all lenders offer it

- ✗ Usually non-refundable

- ✗ Limited to members (credit unions)

Typical cost: $300-$500 one-time fee

When this makes sense: Your auto insurer doesn’t offer gap coverage, or you want it included in your loan for simplicity.

Option 4: Standalone Gap Insurance Companies (Rare, Specialty)

How it works: Third-party companies specifically sell gap insurance, though this is uncommon.

Pros:

- ✓ Sometimes competitive pricing

- ✓ May offer unique terms or coverage

Cons:

- ✗ Another company to deal with during claims

- ✗ Less common, harder to find

- ✗ Must verify legitimacy and reputation

When this makes sense: Rarely. Usually better to go through your auto insurer or credit union.

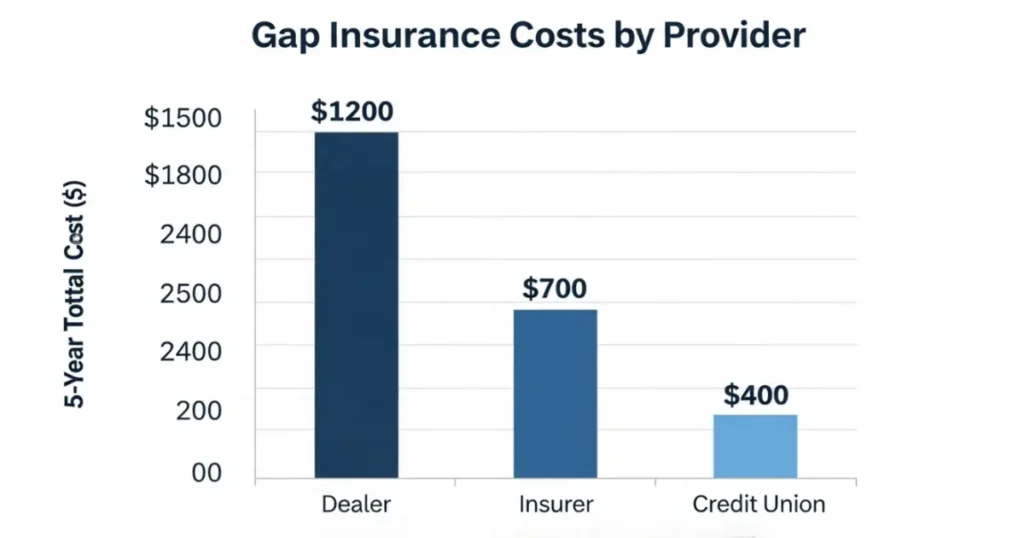

Comparison: Total Cost Over 5 Years

| Source | Cost Structure | Total 5-Year Cost | Cancelable? | Best For |

|---|---|---|---|---|

| Dealership | $600 one-time | $600 + interest (~$720) | Sometimes | Convenience, immediate coverage |

| Auto Insurer | $40/year | $200 | Yes | Budget-conscious, best value |

| Credit Union | $400 one-time | $400 + interest (~$480) | Rarely | Moderate cost, loan bundling |

| Bank | $500 one-time | $500 + interest (~$600) | Rarely | When others unavailable |

Clear winner for most people: Auto insurance company

Gap Insurance vs. New Car Replacement: What’s the Difference?

Understanding New Car Replacement Coverage

New car replacement insurance is similar to gap insurance, but it works differently:

What it covers: If your new car (typically less than one year old and under 15,000 miles) is totaled, new car replacement pays for a brand-new version of the same make and model, not just its depreciated value.

Key differences from gap insurance:

| Feature | Gap Insurance | New Car Replacement |

|---|---|---|

| What it pays | Loan balance minus ACV | Cost of new equivalent vehicle |

| When available | Cost of a new equivalent vehicle | Usually first 1-2 years only |

| Cost | $20-$60/year | $50-$100/year |

| Works with | Any vehicle situation | New cars only (specific age/mileage limits) |

| Pays for | Loan payoff | Vehicle replacement |

Can You Have Both?

Yes, and in some situations, both make sense:

Scenario where both help:

- New car price: $40,000

- Financed with $2,000 down: $38,000 loan

- Car totaled after 8 months

- Current value: $32,000

- New replacement cost: $40,000

With only gap insurance:

- Gap pays: $38,000 (loan) – $32,000 (ACV) = $6,000

- You receive: $32,000 from insurance + $6,000 from gap = $38,000 (loan paid off)

- You have $0 to put toward a replacement

With gap AND new car replacement:

- New car replacement pays: $40,000 (new vehicle cost)

- Gap insurance doesn’t trigger (no gap exists)

- You receive a new equivalent vehicle

Which Should You Choose?

Choose gap insurance if:

- You financed heavily with a small down payment

- Your primary concern is the loan payoff

- You want affordable protection ($20-$60/year)

- Your car is more than 1-2 years old

Choose a new car replacement if:

- Your car is brand new (under 1 year old)

- You made a substantial down payment (positive equity)

- You want a new vehicle if totaled, not just the loan payoff

- You can afford a slightly higher cost ($50-$100/year)

Choose both if:

- Brand new car with heavy financing

- Maximum protection desired

- Combined cost is still reasonable ($70-$160/year total)

Most people should prioritize gap insurance as it addresses the more common risk scenario.

Gap Insurance for Leased Vehicles: Special Considerations

Do I Need Gap Insurance on a Lease?

Usually, no; it’s often included, but you must verify.

Why lessees need gap protection: When you lease, you don’t own the vehicle—the leasing company does. If the car is totaled:

- Insurance pays the car’s actual cash value

- You still owe the remaining lease payments plus the residual value

- The gap can be substantial

The good news: Most lease agreements automatically include gap coverage (sometimes called “lease gap waiver” or “lease protection”) at no extra charge.

What’s Included in Lease Gap Coverage

Lease gap coverage typically pays:

- Difference between ACV and the remaining lease obligation

- Early termination fees

- Security deposit forfeiture

- Disposition fees

- Sometimes, excessive wear-and-tear charges

This is more comprehensive than standard gap insurance.

How to Verify Your Lease Gap Coverage

Check your lease agreement for:

- Clauses mentioning “gap waiver,” “gap protection,” or “total loss protection.”

- Lease inception fees breakdown (look for gap insurance line item)

- Lessor protection provisions

Not clearly stated? Ask your dealer specifically: “Does my lease agreement include gap coverage for total loss? Can you show me where it’s stated in the contract?”

When You Might Need Additional Gap Insurance for Leases

Purchase separate gap insurance if:

- Your lease doesn’t include it (rare but possible with some smaller finance companies)

- You put a large capitalized cost reduction down (big down payment)

- You transferred substantial negative equity into the lease

- The included gap coverage has limitations or exclusions

Cost for lease gap insurance: Similar to purchase gap insurance ($20-$60/year from insurers)

Common Gap Insurance Myths and Misconceptions

Myth 1: “Gap Insurance Covers My Deductible”

Reality: No, gap insurance does not cover your comprehensive or collision deductible. You’re still responsible for that amount.

Example:

- Car value: $25,000

- Deductible: $500

- Insurance payout: $24,500

- Loan balance: $28,000

- Gap covers: $28,000 – $24,500 = $3,500

- You still pay: $500 (your deductible)

Myth 2: “I Can Buy Gap Insurance Anytime”

Reality: Most insurers require you to add gap coverage within 30 days of vehicle purchase or lease. After that window closes, you may be unable to add it.

Exceptions: Some dealers allow you to purchase their gap insurance later, but at a higher cost.

Action item: Decide on gap insurance BEFORE or immediately after buying your vehicle.

Myth 3: “Gap Insurance Covers Mechanical Problems”

Reality: Gap insurance only covers total loss from accidents or theft—not mechanical breakdowns, engine failure, or transmission problems.

What you need for mechanical coverage: an extended warranty or a vehicle service contract (two completely different products).

Myth 4: “Gap Insurance is a Scam or Unnecessary”

Reality: Gap insurance is legitimate, highly regulated, and can save you thousands of dollars. Whether it’s necessary depends on your specific situation.

It’s not a scam, but:

- Dealer markup can be excessive (shop around)

- You might not need it if you made a large down payment

- You should understand what you’re buying

Myth 5: “Gap Insurance Costs Thousands of Dollars”

Reality: Through your auto insurer, gap coverage typically costs $20-$60 per year. Even dealer gap insurance rarely exceeds $700.

Where the confusion comes from: People sometimes confuse gap insurance with extended warranties (which can cost $2,000-$4,000).

Myth 6: “My Regular Car Insurance Includes Gap Coverage”

Reality: Standard auto insurance policies do NOT include gap coverage; it’s always an optional add-on.

What standard insurance covers: Only the actual cash value (current market value) of your vehicle.

You must specifically purchase gap coverage separately.

Myth 7: “Gap Insurance Pays for a New Car”

Reality: Gap insurance pays the difference between your loan balance and your car’s value; it does not buy you a new car.

After a total loss with gap insurance:

- Your loan is paid off

- You receive your insurance settlement

- You’re responsible for purchasing your next vehicle

(Confused with new car replacement coverage, which is different)

Myth 8: “I Can Cancel Anytime and Get a Full Refund”

Reality: Refund policies vary dramatically by provider:

Auto insurer gap coverage: Usually refundable on a pro-rata basis (you get back the unused portion)

Dealer gap insurance: Often non-refundable or partially refundable with restrictions

Always read cancellation terms before purchasing.

How to Cancel Gap Insurance (And Get a Refund)

When You Should Cancel Gap Insurance

Cancel when you:

- Build positive equity: Your car is worth more than you owe

- Pay off your loan: No loan = no gap to cover

- Refinance to a shorter term: Gap risk is eliminated

- Sell or trade the vehicle: No longer own the car

- Total the vehicle: Coverage automatically ends

How to check if you should cancel: Every 6-12 months, compare your loan balance to your car’s current value (check KBB or NADA). Once you have positive equity, gap insurance is unnecessary.

Canceling Dealer Gap Insurance

Process:

- Contact the dealer’s finance department or the gap insurance administrator (listed in your paperwork)

- Request a cancellation form

- Provide required information:

- Gap insurance policy number

- Loan account number

- Current odometer reading

- Reason for cancellation

- Submit the form along with any required documents

Refund calculation: If refundable, typically pro-rata based on remaining time or mileage

Example refund:

- Total cost: $600 for 72-month coverage

- Canceled after 24 months (1/3 of term)

- Refund: $400 (2/3 remaining)

Warning: Some dealer policies are non-refundable or have significant cancellation fees. Check your contract.

Canceling Auto Insurance Gap Coverage

Process:

- Call your insurance agent or the company’s customer service

- Request gap coverage removal from your policy

- Confirm the effective cancellation date

Refund: You’ll receive a pro-rated refund on your next bill or as a separate check

Much simpler than dealer gap cancellation, and most insurers handle it immediately.

Gap Insurance Tax Deductibility and Financial Considerations

Is Gap Insurance Tax Deductible?

For personal vehicles: No, gap insurance premiums are not tax-deductible for personal use vehicles.

For business vehicles: Potentially yes, if you use the vehicle exclusively for business and itemize business expenses. Consult a tax professional for your specific situation.

Financing Gap Insurance: The Hidden Cost

When you finance gap insurance through a dealer (rolling it into your loan), you pay interest on that insurance cost.

Example:

- Gap insurance cost: $600

- Auto loan rate: 6%

- Loan term: 60 months

- Total cost with interest: ~$679

The extra $79 is interest paid on insurance.

Better approach: If you must buy dealer gap insurance, ask if you can pay for it separately (cash or credit card) instead of financing it.

Financial Planning: Gap Insurance as Risk Management

Think of gap insurance as financial disaster prevention:

The risk you’re insuring against:

- Total loss accident: 2-3% annual probability for the average driver

- Gap amount: $3,000-$7,000 potential exposure

- Expected cost of risk: $60-$210/year (2-3% of $3,000-$7,000)

Insurance cost: $20-$60/year

Value proposition: You’re paying $20-$60 to protect against $60-$210 in expected loss, plus the catastrophic risk of owing thousands on a car you can’t drive.

This is excellent risk mitigation.

Real-Life Gap Insurance Stories: When It Saved (and Cost) Drivers

Success Story 1: The New Mom’s Nightmare Avoided

Sarah’s situation:

- Bought a 2023 Honda Pilot for $42,000

- Put $3,000 down, financed $39,000

- Added gap insurance through her auto insurer ($38/year)

What happened: Six months later, Sarah was T-boned at an intersection while her newborn was in the car (both fine). The SUV was totaled.

The numbers:

- Insurance settlement: $36,500 (depreciation hit hard on new SUVs)

- Loan balance: $38,200

- Gap: $1,700

Result: Gap insurance paid the $1,700. Sarah walked away from the accident with her loan paid off, her insurance settlement, and no debt.

Sarah’s reflection: “That $38 I paid for gap insurance saved me from $1,700 in debt during one of the most stressful times of my life. Best $38 I ever spent.”

Success Story 2: The Underwater Trade-In Rescue

Marcus’s situation:

- Traded in a car with $5,000 negative equity

- Rolled that into a new $32,000 truck loan

- Total financed: $37,000

- The dealer convinced him to buy gap insurance ($550)

What happened: Eight months later, his truck was stolen and never recovered.

The numbers:

- Insurance settlement: $28,000 (used truck market was soft)

- Loan balance: $35,500

- Gap: $7,500

Result: Gap insurance paid the $7,500. Marcus was devastated to lose his truck but relieved he wasn’t stuck paying $7,500 for a vehicle he’d never see again.

Marcus’s reflection: “I almost didn’t buy it because $550 seemed steep, but it saved me $7,500. That’s the best return on investment I’ve ever seen.”

Cautionary Story: When Gap Insurance Wasn’t Enough

Jessica’s situation:

- Bought a $28,000 sedan

- Put $0 down, financed $28,000

- Opted for gap insurance through the dealer

What happened: She totaled the car 18 months later.

The problem: Jessica had rolled $3,000 in negative equity from her trade-in, extended warranties ($2,000), and aftermarket accessories ($1,500) into her loan. Her loan balance was actually $34,500.

The numbers:

- Insurance settlement: $19,000 (significant depreciation)

- Loan balance: $32,100

- Gap insurance covered: $13,100

- BUT: Her gap policy excluded the rolled-in negative equity and add-ons

Result: Gap insurance paid the gap on the vehicle itself, but Jessica still owed $2,400 for the old debt and add-ons.

Lesson: Read your gap insurance policy carefully. Some don’t cover rolled-in negative equity or optional products.

Alternatives to Gap Insurance: Other Ways to Protect Yourself

Alternative 1: Make a Larger Down Payment

How it works: Put down 20-30% to start with positive equity and never be underwater.

Pros:

- Eliminates gap risk entirely

- Lower monthly payments

- Less interest paid overall

- No insurance premiums needed

Cons:

- Requires significant upfront cash

- Ties up money that could be invested elsewhere

- Not feasible for many buyers

Who this works for: Buyers with substantial savings who prioritize being debt-free and avoiding risk.

Alternative 2: Choose a Shorter Loan Term

How it works: Finance over 36-48 months instead of 60-72 months to build equity faster.

Pros:

- Pay off principal quickly

- The underwater period is brief (6-18 months)

- Save thousands in interest

- Gap risk minimized

Cons:

- Higher monthly payments

- Less cash flow flexibility

- May limit which vehicles you can afford

Who this works for: Buyers with stable, higher incomes who can afford larger payments.

Alternative 3: Buy a Car That Holds Its Value

How it works: Research and purchase vehicles known for low depreciation.

Best value-holding vehicles (according to recent data):

- Toyota Tacoma, 4Runner, Land Cruiser

- Subaru Outback, Forester, Crosstrek

- Honda CR-V, Ridgeline

- Jeep Wrangler

- Porsche 911 (luxury segment)

- Ford Bronco

Pros:

- Lower overall depreciation means a smaller gap

- Better trade-in value later

- Financial benefits beyond just gap risk

Cons:

- These vehicles often cost more upfront

- Limited selection

- Market conditions can change

Who this works for: Buyers with flexibility in vehicle choice who prioritize long-term value.

Alternative 4: Self-Insure (Build an Emergency Fund)

How it works: Set aside $5,000-$10,000 in savings specifically for potential gap exposure.

Pros:

- No insurance premiums paid

- Money remains yours if the gap event never happens

- Can earn interest on savings

- Total control

Cons:

- Requires substantial savings discipline

- Ties up emergency funds

- If a gap event happens, it depletes savings

- Most people don’t have this cushion

Who this works for: High-income earners with substantial emergency funds who prefer self-insuring risks.

Alternative 5: Pay Down Principal Aggressively

How it works: Make extra principal-only payments to reduce your balance faster than the car depreciates.

Strategy:

- Add $100-200 to each monthly payment

- Make one extra payment per year

- Apply bonuses or tax refunds to principal

Pros:

- Closes the gap quickly

- Reduces total interest paid

- Builds equity faster

- No insurance needed after equity is positive

Cons:

- Requires extra cash flow

- Reduces financial flexibility

- Opportunity cost (could invest money elsewhere)

Who this works for: Buyers with extra cash flow who want to eliminate debt quickly.

None of These Alternatives Are Perfect

The reality: For most car buyers who:

- Finance 80-100% of the vehicle

- Choose 60+ month loan terms

- Buy new or lightly used vehicles

- Don’t have $10,000+ in savings

Gap insurance remains the most practical, affordable protection at $20-$60/year.

State-by-State Gap Insurance Regulations

Gap Insurance Isn’t Available Everywhere

States where gap insurance may be restricted or regulated differently:

- Each state has unique insurance regulations

- Some states require specific disclosure language

- Refund policies are regulated by the state

- Cancellation rights vary

Key State Differences

California: Strict consumer protection laws; dealers must provide clear gap insurance disclosures; pro-rata refunds required

New York: Gap insurance is considered a debt cancellation agreement rather than insurance, regulated by banking law

Florida: Requires specific cancellation provisions in gap contracts

Texas: Gap insurance policies must be filed with the Department of Insurance

Action step: Ask your dealer or insurer about your state’s specific gap insurance regulations and consumer protections.

Conclusion: Making Your Gap Insurance Decision

Here’s what you need to remember: gap insurance is inexpensive protection against a potentially catastrophic financial loss. For most American car buyers who finance heavily, choose long loan terms, or can’t absorb a $5,000 surprise expense, gap insurance is absolutely worth it.

The decision framework is simple:

You definitely need gap insurance if:

- You put less than 20% down

- Your loan term is 60+ months

- You financed 100%+ of the vehicle’s value (rolled in negative equity)

- You bought a new vehicle

- You bought a vehicle with fast depreciation

- You can’t comfortably absorb a $3,000-$7,000 unexpected expense

You probably don’t need gap insurance if:

- You put 30%+ down

- Your loan term is 36 months or less

- You bought a 3+ year old used vehicle

- You have substantial savings specifically for emergencies

- Your vehicle holds its value exceptionally well

The smart buying strategy:

- Before you shop for a vehicle, call your auto insurance company and get a quote for gap coverage, usually $20-$60/year.

- At the dealership, if the finance manager offers gap insurance, compare it to your insurer’s quote. If the dealer’s price is less than $400 and you can’t add it to your auto policy, consider it. If it’s $500+, decline and use your insurer instead.

- Add gap coverage to your auto insurance within 30 days of purchase if you didn’t buy it at the dealer.

- Monitor your equity position annually. Once you have positive equity (the car is worth more than you owe), cancel your gap coverage.

Most common mistake: Paying $600-$900 at the dealer for gap insurance when your auto insurer would charge $100-$200 total over five years. Don’t fall for this. Shop around.

Second most common mistake: Declining gap insurance entirely because “insurance is a scam” or “it won’t happen to me,” then facing a $5,000 debt on a totaled car. Don’t gamble with your financial security.

What is gap insurance? It’s an affordable peace of mind that protects you from the financial nightmare of owing thousands on a car you can’t drive. Do I need gap insurance? If you financed heavily, have a long loan, or can’t easily absorb a major unexpected expense, the answer is almost certainly yes.

The average gap insurance claim is $5,000-$6,000. The average cost through your auto insurer is $150-$250 over five years. That’s a 20:1 to 40:1 return on investment if you need it.

Take action today: If you recently financed a vehicle and don’t have gap coverage, call your auto insurance company this week. If you’re shopping for a car, get that gap insurance quote before you set foot in a dealership. Five minutes of preparation could save you thousands of dollars and massive stress.

Don’t wait until it’s too late. The time to get gap coverage car insurance is now, before you need it.

Frequently Asked Questions

1. What is gap insurance, and how does it work?

Gap insurance (Guaranteed Asset Protection) is optional coverage that pays the difference between what your car is worth and what you still owe on your loan if your vehicle is totaled or stolen. For example, if your car is worth $20,000 but you owe $25,000 on your loan, gap insurance pays the $5,000 difference after your regular auto insurance pays the car’s value. Without gap insurance, you’d be responsible for paying that $5,000 out of pocket for a car you no longer have. Gap insurance only activates when your vehicle is declared a total loss; it doesn’t cover regular repairs, mechanical issues, or your insurance deductible.

2. Do I need gap insurance if I made a down payment?

It depends on how much you put down. If you made a substantial down payment (20-30% or more), you likely don’t need gap insurance because you started with positive equity. However, if your down payment was small (10% or less) or you rolled negative equity from a trade-in into your new loan, you definitely need gap insurance. Even with a moderate down payment of 10-15%, new car depreciation can create a gap in the first 1-2 years. The key question is: if your car were totaled today, would your insurance settlement cover your entire loan payoff? If the answer is no, you need gap insurance. Check your loan balance against your car’s current value (using Kelley Blue Book) to determine your risk.

3. How much does gap insurance cost, and where should I buy it?

Gap insurance costs vary dramatically by provider: dealerships typically charge $400-$700 as a one-time fee (rolled into your loan), while auto insurance companies charge $20-$60 per year, averaging just $3-$5 per month added to your premium. Over five years, that’s $100-$300 from an insurer versus $500-$800 from a dealer. The best option for most people is adding gap coverage to your existing auto insurance policy; it’s significantly cheaper, easily cancelable, and provides the same protection. Credit unions offer a middle ground at $300-$500. Never pay more than $500 at a dealer, and always shop around before accepting their offer.

4. Can I buy gap insurance after I purchase my car?

Yes, but with strict time limits. Most auto insurance companies require you to add gap coverage within 30 days of purchasing or leasing your vehicle. After this window closes, you may be unable to add it through your insurer. Some dealerships allow you to purchase their gap insurance later, but typically at a higher cost and with more restrictions. The best time to secure gap insurance is immediately after (or even before) buying your vehicle. If you missed the 30-day window with your insurer, check with your lender or dealer about late-addition options, but expect to pay more and face stricter approval requirements based on your current loan-to-value ratio.

5. When can I cancel gap insurance and get a refund?

You should cancel gap insurance once you have positive equity, meaning your car is worth more than you owe on your loan. Check this by comparing your loan payoff amount to your car’s current value (on Kelley Blue Book or Edmunds) every 6-12 months. Most people reach positive equity after 24-36 months of payments. To cancel, contact your gap insurance provider directly. If you purchased through your auto insurer, cancellation is simple, and you’ll receive a pro-rated refund immediately. If you bought through a dealer, the process is more complex, and refund policies vary; some policies are non-refundable or have cancellation fees. Review your original gap insurance contract for specific cancellation terms, or you can also cancel if you pay off your loan early, sell the vehicle, or refinance.